The Future of Audit: What Will Audit Firms Look Like in 2030?

Table of Contents

- Why I’m Writing This

- The Current Landscape

- Re-Thinking the Audit

- Inside the Audit Machine

- What Changes for Clients

- What Changes for Auditors

- The Economics of 2030

Why I’m Writing This

AI is reshaping the accounting profession. And not just accounting, the same forces are reshaping law, consulting, healthcare, education, and almost every other profession built on people delivering services. It’s the same services we talk about when we learn about the constituents of GDP in school. This is the part of the pie that is the largest (particularly in western economies). Over the past century, GDP has shifted from predominantly agriculture, to manufacturing, and now to services as the dominant share. Accounting firms sit squarely inside that category.

Pie chart of U.S. GDP in 2023 showing sectors, with 13% professional services including accounting firms.

There are many ways to think about the transformation that AI can bring to Accounting Firms. One is to see AI as an add-on: tools layered onto the existing models and way of doing work. An enabler for workers to do their work faster and to a better quality.

Another is to take a harder path, and ask the question : what if we started from a blank slate?

This article takes that second path. There are two pieces of content that were particularly inspirational for me choosing the title of this article. I bookmarked them the first time I came across them, and I still find myself coming back to them:

1. If I Were to Start a Bank Today, This Is What It Would Look Like

What stood out was the rare mindset of designing an institution from scratch. Most executives never get that chance; they inherit decades of systems, processes, and culture. But AI brings us closer to that luxury than ever before. It is forcing everyone to consider the possibility of ripping everything down and rebuilding their organizations from the ground up.

A talk by Nigel Morris, hosted by Peter Renton

2. AI Leads a Service-as-Software Paradigm Shift- A Research By Joanne Chen and Jaya Gupta at Foundation Capital

This piece reframed AI not as another SaaS tool, but as something that productizes entire services. The critical shift is how to think about market size: the TAM isn’t just the IT spend of customers buying tools, it’s the much larger pool of salaries and service costs tied to people doing the work. The imagination test is: what happens when end-to-end services can be performed almost entirely by AI, with minimal human involvement? This isn’t workflow automation—it’s AI systems solving customer needs directly.

📖 AI Leads a Service-as-Software Paradigm Shift — research by Joanne Chen and Jaya Gupta at Foundation Capital.

Together, these ideas point to the real question: What would the accounting firm of 2030 look like if we built it from scratch, in an AI-native world?

The Current Landscape

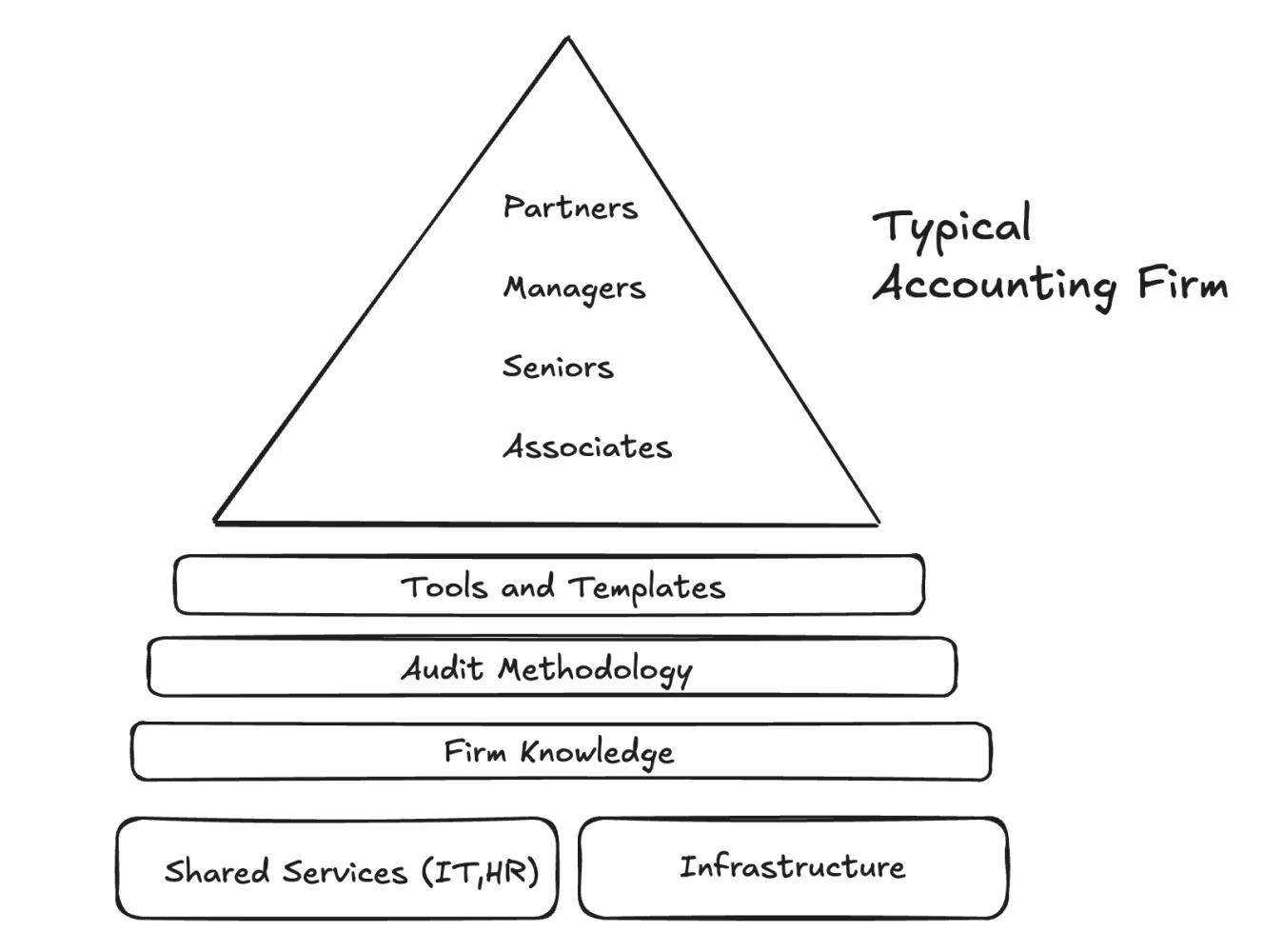

Accounting firms still follow the same pyramid structure that they have always had: partners at the top, managers in the middle, seniors and associates forming the base. And just like before, the pyramid rests on a deep foundation: templates, methodologies, knowledge repositories, infrastructure systems, and the shared services that support the business. Something like this:

Diagram of a typical accounting firm pyramid: partners, managers, seniors, associates, supported by tools, methods, and services.

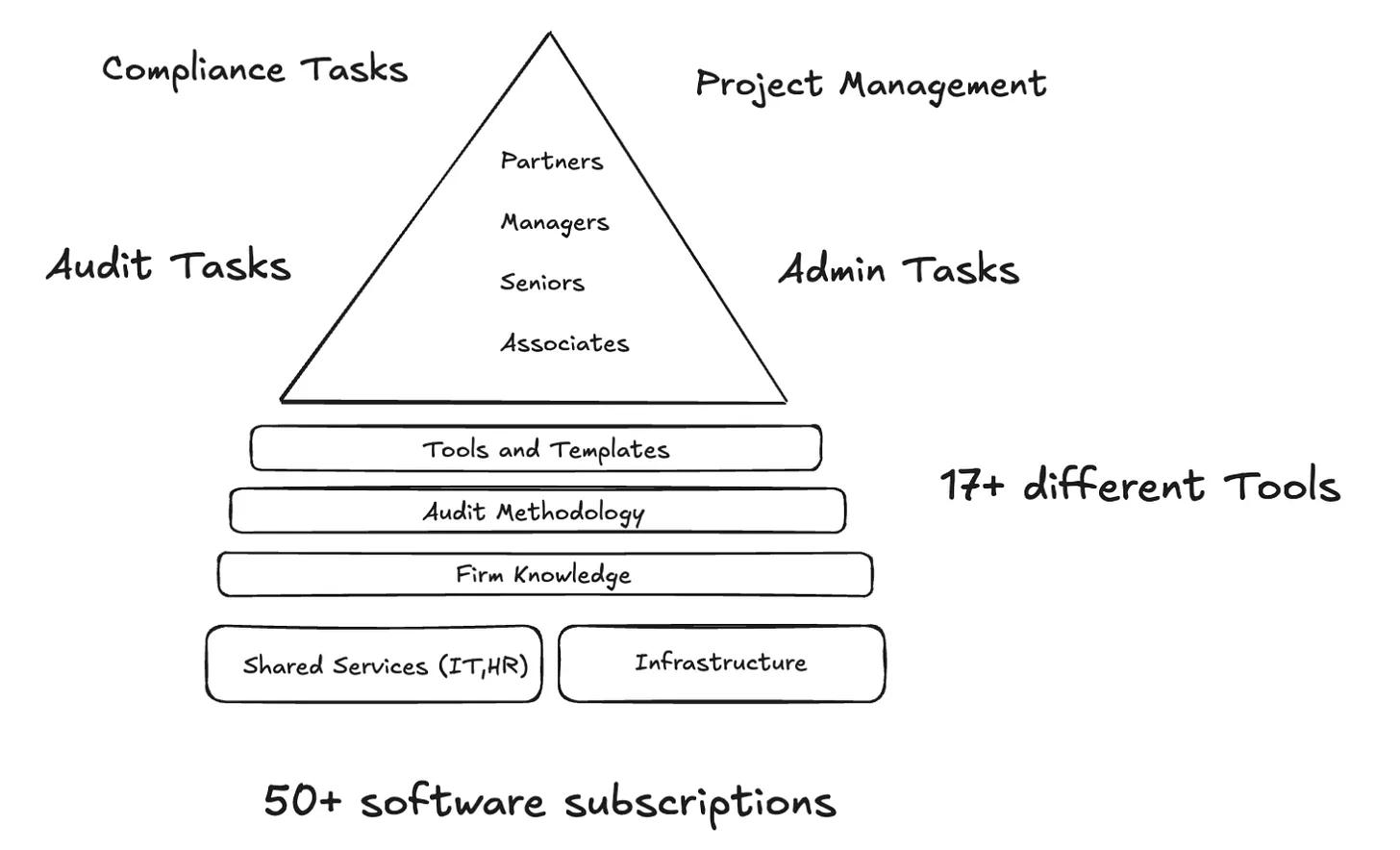

That foundation holds the structure together, but the day-to-day reality is far more complicated. Firms now run 50+ software subscriptions, and people across all levels bounce between tools on average, 17 per person for a single engagement.

- For associates and seniors, this means constant context switching between pulling client data, testing controls, sending confirmations, documenting workpapers, updating workflows, and clearing review notes.

- Managers carry another layer. They live inside scheduling tools, assigning staff across engagements, tracking budgets and timelines, checking status dashboards, and reviewing chunks of work while still doing their share of testing and documentation. They also spend hours coordinating with clients and partners, chasing deliverables, and making sure everything lines up for review.

- Partners add yet another layer of complexity. They juggle oversight across multiple clients, monitor quality and compliance dashboards, allocate resources, review sensitive areas, and handle client relationships. At the same time, they’re pulled into admin tasks like approving expenses, ensuring independence checks are filed, and signing off on compliance requirements.

The result is a patchwork of overlapping tasks across the pyramid: project management, scheduling, resourcing, task management, compliance checks, client communication, and the endless cycle of administrative activities that cut across every level.

From the outside, firms look modern and digital. From the inside, they feel like an old structure resting on a heavy foundation, entangled in dozens of disconnected tools and tasks that demand constant juggling at every level of the pyramid.

Pyramid diagram of a typical accounting firm showing roles, tasks, 17+ tools, and 50+ software subscriptions.

Re-Thinking the Audit

At its core, an audit is about testing whether financial statements can be trusted. Auditors gather client data such as trial balance, general ledger, subledgers, contracts, confirmations etc and then perform procedures: walkthroughs, risk assessments, control testing, substantive testing, analytics, documentation, and ultimately review. The outputs are the familiar ones: the audit opinion, the management letter, and the evidence package behind them.

But that’s only part of the picture. Around this technical work sits a wide layer of project management and administration. Managers allocate staff across jobs, track budgets, update status dashboards, and coordinate schedules with clients. Partners review sensitive areas, oversee quality, and balance resources across multiple engagements. At every level, there are time sheets, compliance requirements, and internal reporting.

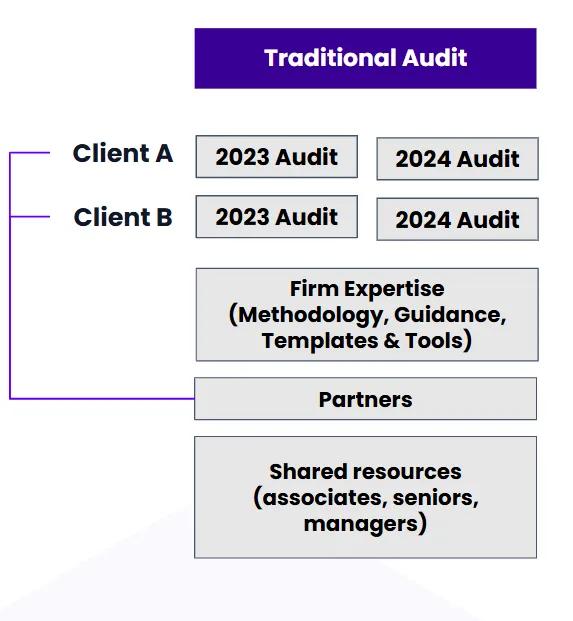

Every audit is also run as a separate project. Each engagement has its own deadlines, team, and deliverables, with managers and partners drawing from a shared pool of people, templates, methodologies, and infrastructure. Around each project orbit the same tasks and tools for data extraction, confirmations, analytics, documentation, scheduling, timesheets, compliance checks. The result is a sprawl where each team essentially rebuilds the same machinery, client by client.

Diagram of a traditional audit showing clients with yearly audits supported by firm expertise, partners, and shared staff resources.

The first instinct is to automate pain points. Digitize checklists, make sampling faster, push timesheets into the background. These are useful steps, they reduce friction and save time. But automation alone just speeds up the same old process. The reason the process looks the way it does is because it was designed for a different era. Paper files made batching and sign-offs essential. Sampling was the only way to make the workload manageable. Review chains evolved to control risk in a manual world. Work was divided into tasks that could be pushed down the pyramid and tracked in hours.

Re-thinking the audit means going further than automation. It means evolving checklists into dynamic procedures that flex to client risk. It means using client data to expand coverage intelligently, not just pick random samples faster. It means building workpapers that link directly to schedules so tie-outs highlight themselves. It means pulling project management out of scattered spreadsheets and portals into a single system.

The shift is about changing both the unit of work and the unit of value. The unit of work moves from people following steps to systems executing policies. The unit of value moves from hours to outcomes: coverage, assurance, readiness. People still sit at the center but their focus shifts to judgment, handling exceptions, advising clients, and telling the story behind the results.

That’s what sets up the next step: imagining the audit not as a chain of manual steps, but as a system, a machine that brings together data, policies, and people in a completely different way.

Inside the Audit Machine

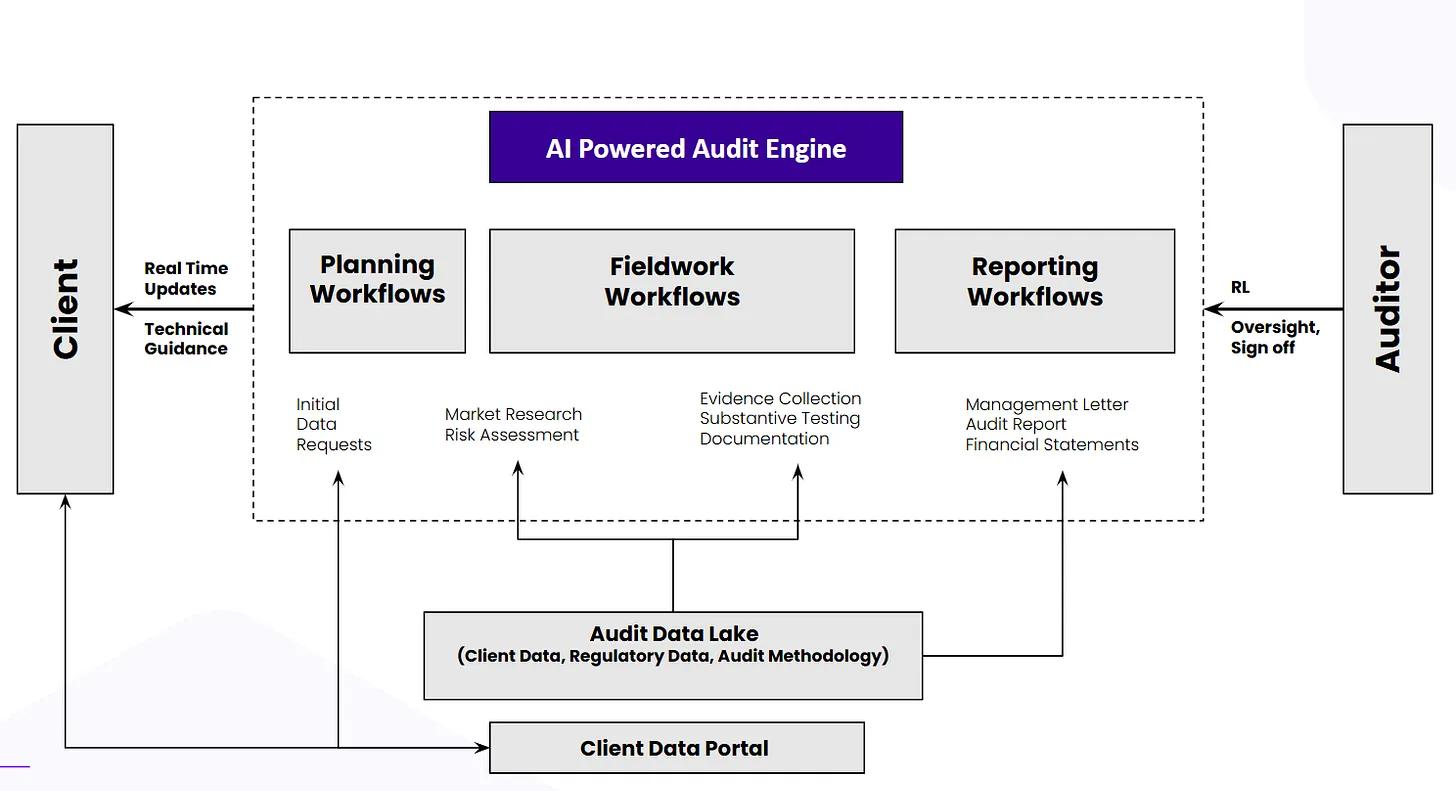

Imagine an AI-Powered Audit Engine where data, policies, and people connect in one system. Clients sit on one side, auditors on the other, and the engine runs in the middle.

The engine is not just about moving data around. It’s about running the audit end-to-end: coordinating requests, executing procedures, tracking progress, assembling evidence, and producing deliverables. What today lives across dozens of tools and checklists is brought together in one integrated environment.

Diagram of an AI-powered audit engine showing client data portal, audit data lake, workflows for planning, fieldwork, reporting, and auditor oversight.

Inside the engine, three categories of workflows operate in sequence but remain connected:

-

Planning

Scoping, risk assessment, materiality, defining procedures, scheduling resources.

-

Fieldwork

Control testing, substantive procedures, confirmations, analytics, documentation.

-

Reporting

Drafting the audit report, preparing the management letter, completing reviews, closing the file.

At each stage, the system handles the operational layer: tracking requests, linking evidence to procedures, surfacing exceptions, and assembling documentation. Instead of being rebuilt from scratch every engagement, these workflows are standardized, consistent, and traceable.

For auditors, the shift is significant. They are still deeply involved—but their role changes. They step in to review, apply judgment, interpret results, and provide technical guidance. They focus more on exceptions, insights, and communication with clients, and less on repetitive coordination. For clients, the experience is clearer requests and better visibility into progress.

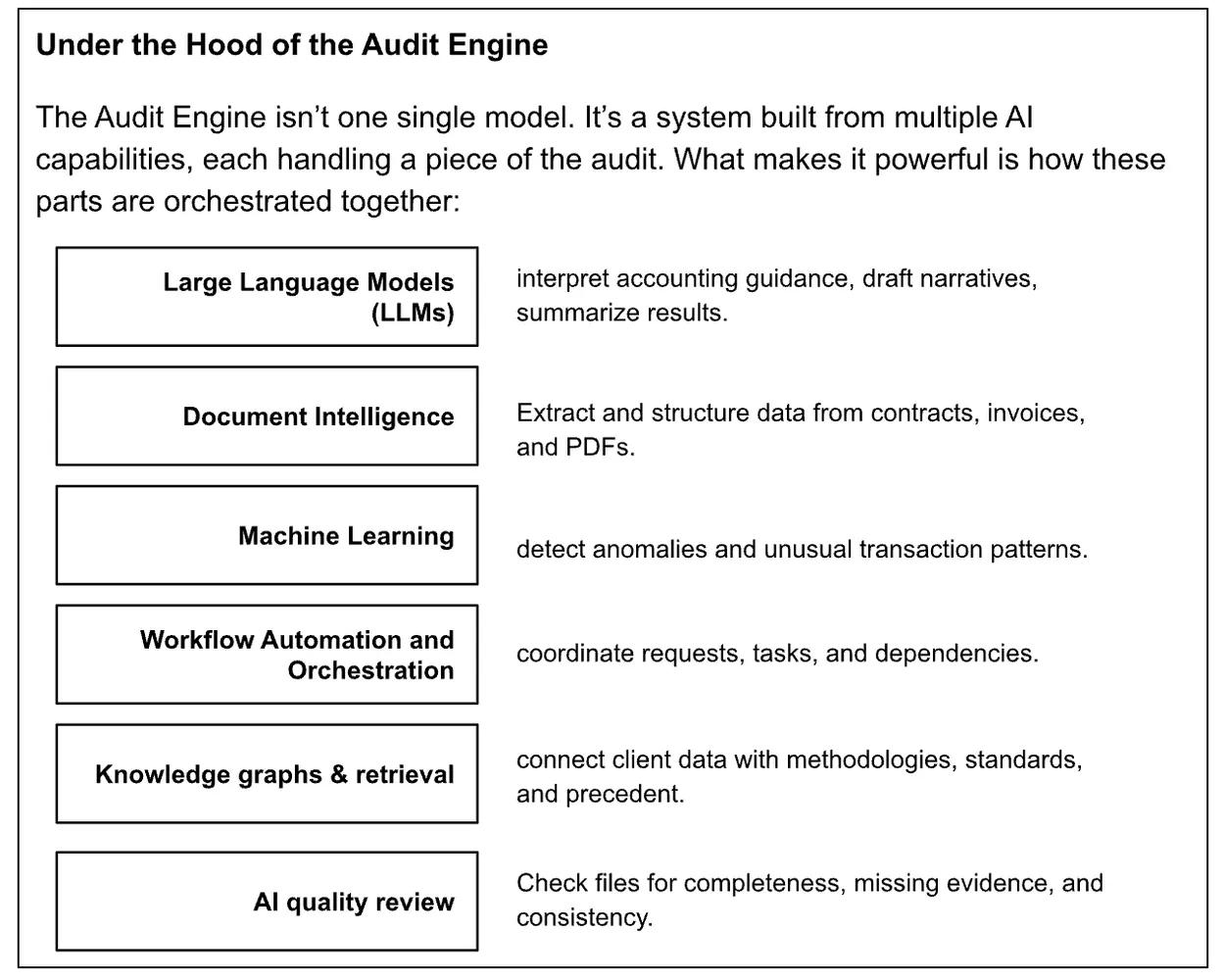

Diagram explaining the AI-powered audit engine, showing LLMs, document intelligence, machine learning, workflow automation, knowledge graphs, and AI quality review.

What Changes for Clients

For clients, today’s audit process often feels heavy. Requests come in through a mix of emails, portals, and spreadsheets. Information is chased down in pieces, with repeated follow-ups when something is missing or inconsistent. Visibility is limited and progress is usually shared in status meetings or near deadlines, not as the work unfolds.

And while many clients ask auditors for insights into their data, controls, and risks, those requests are hard to meet. Most of the firm’s energy is spent on compliance tasks, and tight margins mean there’s little room to go beyond the basics. The result is that clients often see the audit primarily as a cost of doing business rather than a source of value.

With an AI-Powered Audit Engine, the client experience changes in meaningful ways. Requests are clearer and structured, tied directly to the audit procedures they support. If something is missing, the system follows up automatically, auditors don’t have to spend their time chasing. Each document that clients provide is checked by AI as it arrives, so errors like wrong versions or mismatched dates are caught immediately rather than weeks later.

More importantly, clients gain visibility into the process. Instead of waiting for a scheduled call, they can see progress in real time: what’s complete, what’s outstanding, and where exceptions are being investigated. Issues that surface during testing can be flagged earlier, allowing clients to address them before year-end. Along the way, auditors are better positioned to share technical guidance and context, because the engine frees them from the constant drag of coordination and manual checking.

The strategic impact is clear. Clients spend less time on audit admin and more time running their business. Collaboration with auditors is stronger, built on clearer communication and earlier insights. And with the margin pressure on compliance work reduced, auditors have the bandwidth to provide what clients have long been asking for: timely, meaningful insight, not just a compliance report.

What Changes for Auditors

For auditors, much of the day-to-day experience today is defined by repetition and coordination. Associates work through checklists, sample invoices, tie out balances, and compile documentation. Managers spend large portions of their time scheduling staff, tracking tasks, and following up on client requests. Partners juggle budgets, review progress across engagements, and step in to resolve technical or client issues. Across levels, a significant share of time is consumed not by professional judgment, but by the machinery of running the audit.

This is why many auditors feel stretched. Hours are long, budgets are tight, and much of the work is administrative. The space to deliver insight or focus on technical analysis is narrow, squeezed by the pressure to complete files on time and on budget.

With an AI-Powered Audit Engine, the nature of the work begins to change. Routine coordination (requests, reminders, tracking) is handled by the system. Documents are checked automatically as they arrive, flagging issues before they become bottlenecks. AI supports repetitive technical tasks like sampling, extracting key terms from contracts, or drafting first versions of memos. Orchestration ensures that tasks flow logically, reducing the constant context switching that comes with fragmented tools.

The role of the auditor shifts to where human judgment matters most. Associates spend more time investigating exceptions and understanding the story behind the data. Managers focus on interpreting results, guiding staff, and communicating with clients, rather than chasing tasks. Partners concentrate on technical guidance, quality, and delivering insights, rather than firefighting project logistics.

Strategically, this means the profession can start to rebalance. Less grind, more focus on developing expertise. Less time spent on admin, more time adding value for clients. By reducing the weight of low-value tasks, the Audit Engine creates the room for auditors to do what they are trained for, to apply judgment, deliver insight, and build trust.

The Economics of 2030

Behind all of this is economics. The traditional pyramid model relies on layers of people, with margin squeezed out of junior hours. That model is under pressure: clients resist rising fees, staff expect more, and inefficiencies across tools and admin eat into profitability.

One of the most overlooked drivers of margin pressure is employee turnover. Audit has long suffered from high attrition—new hires cycle in, get trained, and often leave after only a few busy seasons. Each departure creates costs: recruiting, onboarding, training, and rework when knowledge walks out the door. Beyond dollars, it creates instability for clients and stress for teams. Firms spend enormous energy backfilling talent just to keep the pyramid standing.

An AI-Powered Audit Engine has the potential to rebalance these economics. By automating repeatable tasks, firms are less dependent on constant waves of junior staff. The system can reduce the drag of inefficiencies and hidden costs tied to turnover. It may also make the work itself more sustainable, giving auditors more time for judgment and insight—factors that could improve retention.

The long-term impact on margins is uncertain. Some firms may capture efficiencies directly, others may choose to reinvest those savings into client value or pricing. What’s clearer is that the cost structure itself changes: less tied to headcount churn, less fragile to inefficiency, and more scalable through systems rather than people alone.

For clients, this means more continuity. For firms, it means greater resilience in a model that has been stretched thin. And for the profession, it opens the door to a future where the economics of audit are not defined only by hours, but by outcomes and trust.